Schedule Balance Sheet in ITR-3: The Ultimate Guide for Indian Businesses & Professionals

Master the Schedule Balance Sheet in ITR-3 with this comprehensive guide. Learn who needs to file, understand the structure, get step-by-step instructions, avoid common errors, and ensure accurate tax filing for your business or profession in India.

The Income Tax Return (ITR) is an annual financial statement that individuals and businesses file with the Income Tax Department of India. For certain taxpayers, especially those engaged in business or profession, ITR-3 is the designated form. A crucial component of ITR-3 is the Schedule Balance Sheet, a snapshot of your financial position at the end of the fiscal year.

This guide aims to demystify the process of preparing and filing the Schedule Balance Sheet in ITR-3. We'll cover everything from understanding the basics to ensuring accurate reporting, enabling you to confidently navigate this important tax filing requirement.

Who Needs to File the Schedule Balance Sheet in ITR-3?

The Schedule Balance Sheet within ITR-3 is a mandatory requirement for specific taxpayers whose financial activities necessitate detailed reporting. Let's break down the categories:

1. Individuals and Hindu Undivided Families (HUFs) with Income from Business or Profession:

- Proprietors: If you are the sole owner of a business (sole proprietorship) or practice a profession (doctor, lawyer, consultant, etc.), and your income is generated from these activities, you are required to file ITR-3 and include the Schedule Balance Sheet. This is regardless of whether your business is audited or not.

- Income Threshold: This requirement applies even if your total income is below Rs. 50 lakhs.

2. Partners in a Firm:

- Income from Firm: If you are a partner in a firm (partnership firm, LLP, etc.) and the firm's income is taxable, you must file ITR-3. The Schedule Balance Sheet is essential to report your share of the firm's assets and liabilities.

- Audit Status: Whether the firm is subject to a tax audit or not, partners are still required to furnish the Schedule Balance Sheet in their individual ITR-3.

Exemptions:

While the above categories generally require filing the Schedule Balance Sheet, there are a few exceptions:

- Individuals/HUFs with Income Below Rs. 50 Lakhs and No Audit: If your total income is less than Rs. 50 lakhs and your business/profession is not subject to a tax audit, you may be exempt from filing the Schedule AL (Assets and Liabilities), which is a similar form to the Schedule Balance Sheet. However, you are still required to report your assets and liabilities in other parts of ITR-3.

- Salaried Individuals: Salaried individuals generally do not need to file the Schedule Balance Sheet unless they have income from other sources like capital gains or house property.

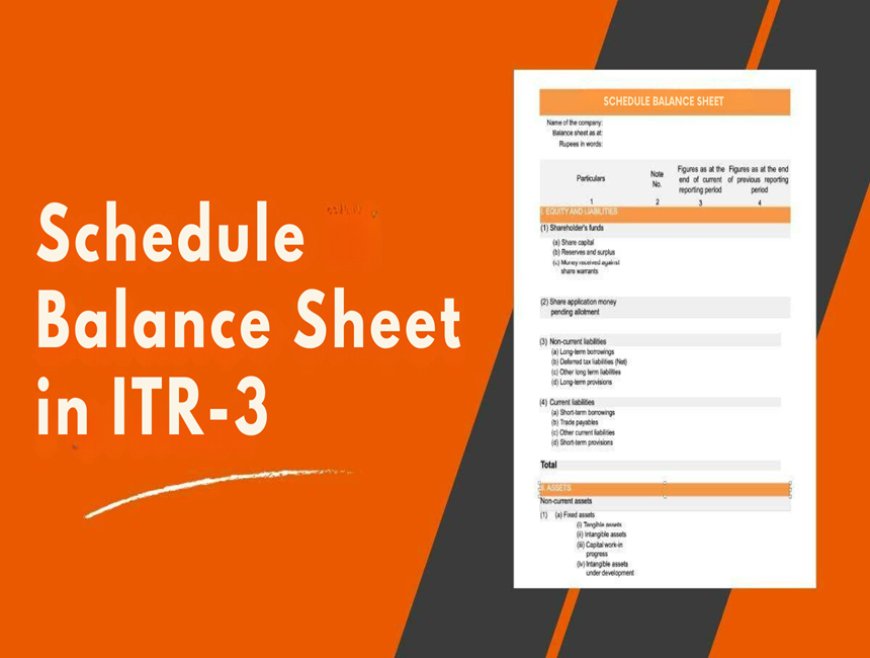

Understanding the Schedule Balance Sheet

The Schedule Balance Sheet is now divided into three parts:

1. Source of Funds: This part is split into four sections:

a) Proprietor's Fund:

- Proprietor's Capital: This represents the owner's investment in the business or profession, including the initial capital contributed and any subsequent additions. It's the core equity of the business owned by the proprietor.

- Reserves and Surplus: This encompasses various types of reserves that are set aside from profits for specific purposes or to strengthen the financial position of the business. Some common reserves include:

- Revaluation Reserve: Created when fixed assets are revalued upwards to reflect their current market value.

- Capital Reserve: Formed from capital profits (gains made from selling assets, receiving premiums on shares, etc.) and cannot be distributed as dividends.

- Statutory Reserve: Mandated by law for certain types of businesses, like banking and insurance.

- General Reserve: A free reserve that can be used for any purpose deemed fit by the business.

- Other Reserves: This category includes any other reserves not specifically mentioned above.

b) Loan Funds:

- Secured Loans: These are loans that are backed by collateral, usually an asset of the business like property, machinery, or inventory. The lender has a legal claim on the collateral in case the borrower defaults on the loan.

- Foreign Currency Loans: Secured loans taken in a foreign currency, which may be subject to exchange rate fluctuations.

- Rupee Loans: Secured loans taken in Indian Rupees (INR).

- Unsecured Loans: These are loans that are not backed by any specific collateral. They are usually granted based on the borrower's creditworthiness and financial standing. Unsecured loans can be from:

- Banks: Formal loans from financial institutions.

- Other Sources: Informal loans from friends, family, or private lenders.

c) Deferred Tax Liability:

- Tax Timing Differences: This arises due to differences in how revenues and expenses are recognized for accounting purposes versus tax purposes. For example, depreciation might be calculated differently under accounting standards and tax laws.

- Future Tax Payments: Deferred tax liability represents the amount of taxes that the business is expected to pay in future periods when these temporary differences reverse.

d) Advances:

-

- Specified Persons (Section 40A(2)(b)): This includes advances received from persons or entities specified under Section 40A(2)(b) of the Income Tax Act. These are typically related parties like relatives or associated enterprises.

- Others: This category encompasses advances received from any other sources, including customers, clients, or other business partners.

2. Application of Funds: This part is split into four sections:

a) Fixed Assets:

This section is dedicated to tracking the business's long-term assets, which are not intended for sale but are used to generate revenue. It's further divided into:

- Gross (Block) Fixed Assets: The original cost of all fixed assets owned by the business, including land, buildings, machinery, equipment, vehicles, furniture, and fixtures. This is the historical value without accounting for depreciation.

- Depreciation: The cumulative reduction in the value of fixed assets due to wear and tear, obsolescence, or other factors. It is an accounting expense that spreads the cost of an asset over its useful life.

- Net (Block) Fixed Assets: This is the Gross Block value minus the accumulated depreciation. It represents the carrying value or book value of the fixed assets.

- Capital Work-in-Progress (CWIP): This includes the costs incurred for ongoing construction or improvement of fixed assets that are not yet ready for use. Once completed, these costs are transferred to the Gross Block of Fixed Assets.

b) Investments:

This section records the value of investments made by the business in various financial instruments. It's further categorized into:

- Long-Term Investments: Investments that are intended to be held for more than one year. This includes:

- Government Securities: Debt instruments issued by the government.

- Other Securities (Quoted and Unquoted): Shares, bonds, debentures, and other securities listed or not listed on stock exchanges.

- Short-Term Investments: Investments that are intended to be held for less than one year. This includes:

- Equity Shares: Ownership shares in companies.

- Preference Shares: Shares with preferential rights to dividends and repayment of capital.

- Debentures: Unsecured debt instruments issued by companies.

c) Current Assets, Loans, and Advances:

This section encompasses a wide range of assets and liabilities that are expected to be realized or settled within one year. It's further divided into:

- Current Assets:

- Inventories: Raw materials, work-in-progress, and finished goods held for sale.

- Sundry Debtors: Amounts owed to the business by customers for goods or services sold on credit.

- Cash and Bank Balances: Cash on hand, bank deposits, and other liquid assets.

- Other Current Assets: Any other assets not specifically mentioned above, such as prepaid expenses or marketable securities.

- Loans and Advances:

- Advances Recoverable: Amounts given as advance payments for goods, services, or other purposes, which are expected to be recovered in cash or in kind.

- Deposits: Money placed with financial institutions or other entities to earn interest or secure a future transaction.

- Loans and Advances to Corporates and Others: Loans given to companies or individuals for various purposes.

- Balance with Revenue Authorities: Amounts deposited with tax authorities for advance tax or other tax-related purposes.

- Current Liabilities and Provisions:

- Sundry Creditors: Amounts owed by the business to suppliers or other parties for goods or services purchased on credit.

- Liability for Leased Assets: Obligations related to leased assets, including lease payments and any outstanding balances.

- Interest Accrued: Interest expense that has been incurred but not yet paid.

- Provisions: Amounts set aside for anticipated expenses or losses, such as provisions for income tax, leave encashment, gratuity, or bad debts.

d) Miscellaneous Expenditure, Deferred Tax Asset, and Profit and Loss Account:

This section includes:

- Miscellaneous Expenditure Not Written Off or Adjusted: Expenses that have been incurred but not yet accounted for in the profit and loss account.

- Deferred Tax Asset: An asset that arises due to timing differences between accounting and tax regulations, representing future tax benefits.

- Profit and Loss Account/Accumulated Balance: The net profit or loss for the year, which is transferred to the balance sheet and added to or subtracted from the retained earnings.

3. No Account Case: A Simplified Approach for Certain Taxpayers

The Income Tax Act of 1961 mandates that businesses and professionals maintain proper books of accounts. However, it recognizes that not all taxpayers might have the resources or expertise to do so. The "No Account Case" section is designed for such taxpayers who do not maintain regular books of accounts.

Eligibility:

To be eligible for the "No Account Case" section, you must meet the following criteria:

- Individual or HUF: You must be an individual or a Hindu Undivided Family (HUF).

- Business Income Below Threshold: Your total income from business or profession should not exceed ₹2 crores in the relevant financial year.

- No Presumptive Taxation Scheme: You should not be opting for any presumptive taxation scheme under sections 44AD, 44ADA, or 44AE of the Income Tax Act.

Details to be Reported:

If you qualify for the "No Account Case," you need to provide the following details in the Schedule Balance Sheet:

-

Total Sundry Debtors: This refers to the total amount owed to your business by customers or clients for goods or services sold on credit.

-

Total Sundry Creditors: This represents the total amount your business owes to suppliers or other parties for goods or services purchased on credit.

-

Value of Stock-in-Trade: This is the value of all goods held by your business for the purpose of sale or manufacture. It includes raw materials, work-in-progress, finished goods, and goods in transit.

-

Cash Balance: This includes all cash on hand and deposits in bank accounts at the end of the financial year.

Benefits:

-

Simplified Reporting: The "No Account Case" section offers a simplified way to report your financial position, especially if you do not have formal accounting records.

-

Reduced Compliance Burden: It relieves you from the detailed reporting requirements applicable to those maintaining regular books of accounts.

Drawbacks:

-

Limited Deductions: You may not be able to claim certain deductions that are available to taxpayers maintaining regular books of accounts.

-

Higher Scrutiny: Your return might be subject to increased scrutiny by tax authorities due to the lack of formal accounting records.

Step-by-Step Guide to Filing Schedule Balance Sheet in ITR-3

Step 1: Gather Your Financial Documents:

a) Audited Balance Sheet:

- Purpose: This is the cornerstone of the Schedule Balance Sheet, as it provides a snapshot of your financial position at the end of the financial year.

- Details: It lists all your assets (what you own) and liabilities (what you owe) and their respective values. Ensure that the balance sheet you have is for the correct financial year and has been audited (if applicable).

- Key Sections: Pay close attention to the figures for fixed assets, investments, current assets, loans & advances, sundry debtors, sundry creditors, and capital accounts.

b) Profit and Loss (P&L) Account:

- Purpose: This statement shows your income and expenses for the financial year, giving a clear picture of your financial performance.

- Details: It includes details of your gross revenue, cost of goods sold, operating expenses, and net profit or loss.

- Key Sections: Focus on the figures for sales/revenue, direct expenses, indirect expenses, and the final net profit/loss figure.

c) Loan Statements:

- Purpose: If you have any outstanding loans (secured or unsecured), you'll need the latest statements to accurately report the loan amounts and interest accrued.

- Details: Loan statements typically show the outstanding principal amount, interest rate, repayment schedule, and any outstanding interest.

- Key Sections: Note down the outstanding loan balances at the end of the financial year for both secured and unsecured loans.

d) Investment Statements:

- Purpose: If you've made any investments (stocks, bonds, mutual funds, etc.), you'll need statements that show their value as of the last day of the financial year.

- Details: Investment statements typically list the investments held, their purchase price, current market value, and any dividends or interest earned.

- Key Sections: Focus on the market value of your investments at the year-end, as this will be reported in the Schedule Balance Sheet.

e) Advance Receipts:

- Purpose: If you've received any advances from customers, clients, or specified persons (as per Section 40A(2)(b)), you'll need proof of these receipts.

- Details: This could include invoices, contracts, bank statements, or any other documents that confirm the receipt of advances.

- Key Sections: Note down the total amount of advances received and outstanding at the end of the financial year.

Additional Documents (If Applicable):

- Deed of Partnership: If you are a partner in a firm, you might need the partnership deed to determine your share in the firm's assets and liabilities.

- Bank Statements: These can help you reconcile your cash balance and track any loan transactions.

- Other Supporting Documents: Any other documents relevant to your business or profession that can substantiate the figures reported in the Schedule Balance Sheet.

Step 2: Navigate to the Schedule Balance Sheet:

a) Access the Income Tax E-filing Portal:

- Go to the official Income Tax Department e-filing website (

https://www.incometax.gov.in/iec/foportal/ - Log in using your user ID (PAN) and password. If you haven't registered yet, create an account first.

b) Start Filing ITR-3:

- Once logged in, navigate to the 'e-File' tab and select 'Income Tax Return.'

- Choose the assessment year (e.g., 2024-25) and select 'ITR-3' as the form type.

- You can either download the offline utility or use the online filing option.

c) Locate Part A-BS:

- The ITR-3 form is divided into various parts (Part A - General, Part A-BS, Part A-P&L, etc.).

- Scroll down or use the navigation panel to find "Part A-BS." This section is specifically for the Balance Sheet details.

d) Find the Schedule Balance Sheet:

- Within Part A-BS, you'll find several sub-sections like "Source of Funds," "Application of Funds," and "No Account Case" (if applicable).

- The entire collection of these sub-sections constitutes the "Schedule Balance Sheet."

Step 3: Part A-BS: Source of Funds (Detailed Instructions)

This section of the Schedule Balance Sheet in ITR-3 aims to capture all the sources from which your business or profession received funds during the financial year. Here's a comprehensive breakdown:

1. Proprietor's Fund:

-

Proprietor's Capital (Opening Balance):

- Enter the balance in the proprietor's capital account as it stood at the beginning of the financial year (April 1st). This is the amount of capital invested by the owner at the start of the year. You can find this figure in your previous year's balance sheet.

-

Additions to Capital:

- This includes any fresh capital introduced into the business by the proprietor during the year. It could be in the form of:

- Additional cash investments

- Assets transferred to the business

- Profits from previous years plowed back into the business

- This includes any fresh capital introduced into the business by the proprietor during the year. It could be in the form of:

-

Deductions from Capital (Drawings):

- This represents any withdrawals made by the proprietor from the business for personal use during the year. It includes cash withdrawals, goods taken for personal use, or any expenses paid by the business on behalf of the proprietor.

-

Total Proprietor's Fund (Closing Balance):

- This is calculated as: Opening Balance + Additions - Deductions. It reflects the proprietor's total capital invested in the business at the end of the financial year.

b) Loan Funds:

-

Secured Loans:

- Foreign Currency Loans: Enter the closing balance (outstanding amount) of any loans taken in foreign currency and secured against an asset of the business.

- Rupee Loans (From Banks and Others): Enter the closing balance of all rupee-denominated loans that are secured against any asset of the business. This includes loans from banks as well as other financial institutions or individuals.

-

Unsecured Loans (including deposits):

- From Banks: Enter the closing balance of any unsecured loans taken from banks.

- From Others: Enter the closing balance of any unsecured loans taken from sources other than banks, including individuals, friends, family, or other entities. This also includes deposits received from others.

-

Total Loan Funds:

- Add up all the closing balances of secured and unsecured loans to arrive at the total loan funds utilized by your business.

c) Deferred Tax Liability:

- Balance at the Year's End:

- Enter the closing balance of any deferred tax liability that exists as of March 31st (the end of the financial year). This figure is usually calculated by your accountant and can be found in your audited balance sheet.

d) Advances:

- From Specified Persons (Section 40A(2)(b)):

- Enter the closing balance of any advances received from persons or entities specified in Section 40A(2)(b) of the Income Tax Act. These typically include relatives, partners, or associated enterprises.

- From Others:

- Enter the closing balance of any other advances received during the year. This could be from customers, clients, or other business associates.

Step 4: Part A-BS: Application of Funds (Detailed Instructions)

This section of the Schedule Balance Sheet in ITR-3 provides a snapshot of how your business or profession has utilized its funds during the financial year. Here's an in-depth explanation of each sub-section:

a) Fixed Assets:

-

Gross Block of Fixed Assets:

- This represents the original cost of all tangible fixed assets owned by your business. It includes the purchase price of assets like land, buildings, machinery, equipment, vehicles, furniture, and fixtures.

-

Less: Depreciation:

- Subtract the cumulative depreciation charged on these fixed assets until the end of the financial year. Depreciation is an accounting method that spreads the cost of an asset over its useful life.

-

Net Block of Fixed Assets:

- This is the value of your fixed assets after deducting accumulated depreciation. It reflects the current book value of these assets.

-

Capital Work-in-Progress (CWIP):

- Enter the total cost incurred on any ongoing construction or improvement projects related to fixed assets that are not yet complete or put to use.

b) Investments:

-

Long-Term Investments:

- Government Securities: Report the closing balance (market value) of all government securities (bonds, treasury bills, etc.) held by your business.

- Other Securities (Quoted and Unquoted): Enter the closing balance of investments in shares, bonds, debentures, and other securities, whether they are listed on stock exchanges (quoted) or not (unquoted).

-

Short-Term Investments:

- Equity Shares: Report the closing balance of investments in equity shares of other companies.

- Preference Shares: Enter the closing balance of investments in preference shares of other companies.

- Debentures: Report the closing balance of investments in debentures issued by other companies.

c) Current Assets, Loans, and Advances:

- Current Assets:

-

- Inventories: Report the value of raw materials, work-in-progress, finished goods, and stock-in-trade held by your business at the end of the financial year.

- Sundry Debtors: Enter the total amount receivable from customers or clients for goods sold or services rendered on credit.

- Cash and Bank Balances: Report the combined balance of cash on hand and deposits in various bank accounts.

- Other Current Assets (Loans and Advances): Include any other assets that are expected to be converted into cash within one year, such as prepaid expenses or short-term investments not covered above.

- Loans and Advances Given:

-

- Advances Recoverable in Cash or Kind: Report the amount of advances given to employees, suppliers, contractors, or others, which are expected to be recovered in cash or kind.

- Deposits: Include fixed deposits or other deposits made with banks or other financial institutions.

- Loans and Advances to Corporates and Others: Enter the amount of loans given to companies, firms, or individuals.

- Balance with Revenue Authorities: Report any amount deposited with tax authorities as advance tax or other payments.

- Current Liabilities and Provisions:

-

- Sundry Creditors: Enter the total amount payable to suppliers or other parties for goods or services purchased on credit.

- Liability for Leased Assets: If your business leases assets, report the outstanding liability at the year's end.

- Interest Accrued (but not due) on Loans: Include the interest expense that has been incurred but not yet paid on various loans.

- Provisions: Report any amounts set aside for anticipated expenses or losses, such as provisions for income tax, gratuity, leave encashment, etc.

Step 5: Part A BS– No Account Case (If Applicable):

This section is exclusively for taxpayers who are NOT maintaining formal books of accounts. It's designed to simplify reporting for certain individuals and Hindu Undivided Families (HUFs) engaged in business or profession.

Eligibility:

To qualify for the No Account Case, you must fulfill ALL of the following conditions:

-

Income Threshold: Your total income from business or profession should not exceed ₹2 crores in the relevant financial year.

-

Not Opted for Presumptive Taxation: You should not have opted for any presumptive taxation scheme under sections 44AD, 44ADA, or 44AE of the Income Tax Act.

-

Individual or HUF: You must be filing ITR-3 as an individual or an HUF.

Information Required:

If you meet the above criteria, you'll need to provide the following information in Part A BS – No Account Case:

-

Total Sundry Debtors:

- This refers to the total amount owed to your business by your customers or clients for goods or services sold on credit.

- Essentially, it's the total amount you expect to receive from your customers in the future.

-

Total Sundry Creditors:

- This represents the total amount your business owes to suppliers or other parties for goods or services purchased on credit.

- It's the total amount you need to pay to your suppliers in the future.

-

Value of Stock-in-Trade:

- This is the total value of all goods held by your business for the purpose of sale or manufacture at the end of the financial year.

- It includes raw materials, work-in-progress, finished goods, and goods in transit.

- It's important to value your stock accurately, either at cost price or market price, whichever is lower.

-

Cash Balance:

- This includes the total amount of cash you have on hand, as well as the balances in all your bank accounts, as of the end of the financial year.

Step 6: Review and Cross-Check – The Key to Accuracy

This is perhaps the most critical step in the entire ITR-3 filing process. Errors in the Schedule Balance Sheet can lead to scrutiny, delays, and even penalties. Here's a detailed breakdown of the review process:

-

Data Accuracy:

- Double-Check Every Entry: Scrutinize every figure you've entered in the Schedule Balance Sheet. Ensure they match the corresponding values in your audited balance sheet and profit and loss account.

- Typos and Transposition Errors: Look out for simple mistakes like typos or accidentally swapping digits (e.g., entering 1234 instead of 1243).

- Zeroes and Decimal Places: Pay close attention to the placement of zeroes and decimal points, as these can significantly impact the reported amounts.

- Foreign Currency Conversions: If you have any foreign currency loans or investments, ensure they are converted to Indian Rupees (INR) using the correct exchange rate as per RBI guidelines.

-

Consistency:

- Balance Sheet Reconciliation: The figures reported in the Schedule Balance Sheet should perfectly match the corresponding figures in your audited balance sheet. This includes the totals for assets, liabilities, and capital.

- P&L Account Reconciliation: Similarly, the income and expense figures in the Schedule Balance Sheet should match those in your profit and loss account.

- Inter-Section Consistency: Ensure consistency within the Schedule Balance Sheet itself. For example, the total of all sources of funds should equal the total of all applications of funds.

-

Calculations:

- Recalculate Totals: Don't rely solely on the auto-calculation features of the e-filing portal or offline utility. Manually recalculate all totals and subtotals to ensure accuracy.

- Depreciation: Double-check the depreciation figures used for fixed assets. They should align with the depreciation method and rates prescribed by the Income Tax Act.

- Interest Calculations: Verify the interest accrued on loans and deposits to ensure they are calculated correctly.

Additional Tips:

- Fresh Eyes: After completing the review yourself, ask a colleague, friend, or family member to take a look. A fresh pair of eyes might catch something you missed.

- Print and Review: If possible, print out the filled Schedule Balance Sheet and review it on paper. This can sometimes make errors more apparent.

- Consult Your CA: If you have any doubts or complex situations, don't hesitate to seek professional guidance from your Chartered Accountant.

Step 7: File Your ITR-3

Once you're confident that your Schedule Balance Sheet is accurate and complete, you can proceed with filing your ITR-3:

-

Upload the ITR-3:

- If using the offline utility, generate the XML file and upload it to the e-filing portal.

- If filing online, simply save your progress and proceed to the next step.

-

Pay Taxes Due (If Any):

- If you have any outstanding tax liability, pay it online through the e-filing portal using the available payment options.

-

E-verify Your Return:

- E-verification is mandatory to complete the filing process. You can e-verify using your Aadhaar OTP, net banking, bank account number, Demat account, or other methods available on the portal.

Common Mistakes to Avoid When Filing Schedule Balance Sheet in ITR-3

Accurate and meticulous reporting in the Schedule Balance Sheet is crucial for a smooth tax filing process and to avoid potential scrutiny from tax authorities. Here are the common pitfalls to watch out for and how to avoid them:

1. Inaccurate Data Entry:

- Double-Check Figures: The most common mistake is simply entering incorrect numbers. Always double-check each figure you enter in the Schedule Balance Sheet against your audited financial statements (balance sheet and P&L account).

- Verify Totals: Ensure that the totals you calculate in the Schedule Balance Sheet (e.g., total assets, total liabilities) match the totals in your financial statements.

- Transposition Errors: Be careful not to accidentally switch digits while entering numbers (e.g., entering 52 instead of 25).

2. Incomplete Reporting:

- Omitting Assets or Liabilities: Don't leave out any assets or liabilities, even if they seem small or insignificant. This includes assets held overseas, investments in other companies, or loans given to friends or family.

- Forgetting Accrued Expenses: Remember to include accrued expenses (expenses incurred but not yet paid) and accrued income (income earned but not yet received) as per your financial statements.

- Ignoring Contingent Liabilities: Contingent liabilities are potential obligations that may arise depending on the outcome of a future event. Disclose these in the relevant section of the balance sheet if they are material.

3. Incorrect Classification:

- Misclassifying Assets and Liabilities: Ensure you classify each item correctly as a fixed asset, investment, current asset, loan & advance, current liability, or provision. This is crucial for accurate reporting and analysis of your financial position.

- Confusing Short-Term and Long-Term: Be careful to distinguish between short-term (current) and long-term assets and liabilities. Current assets and liabilities are those that are expected to be realized or settled within one year.

4. Ignoring Professional Guidance:

- Complex Situations: If you encounter any complex financial transactions or have doubts about how to report certain items, don't hesitate to seek help from a qualified Chartered Accountant (CA).

- Tax Laws: Tax laws can be intricate, and a CA can ensure that your Schedule Balance Sheet complies with all the relevant regulations.

Consequences of Incorrect Filing of Schedule Balance Sheet in ITR-3

Accurate and complete reporting in the Schedule Balance Sheet is not just a formality; it's a legal obligation. Mistakes or deliberate misrepresentations can have serious repercussions for taxpayers. Here's a detailed look at the potential consequences:

1. Tax Scrutiny and Assessment:

- Increased Scrutiny: An incorrectly filled Schedule Balance Sheet can raise red flags and trigger a tax scrutiny. This means your return will be subjected to a detailed examination by the Income Tax Department.

- Detailed Inquiries: Tax officials may ask you to provide additional information, explanations, and supporting documents to verify the details in your Schedule Balance Sheet.

- Extended Assessment Period: Scrutiny can prolong the assessment process, leading to delays in receiving any tax refunds or resolving tax-related issues.

2. Interest and Penalties:

- Underreporting Income: If you understate your income or omit certain assets in the Schedule Balance Sheet, you may be liable to pay additional taxes on the undeclared income.

- Overstating Expenses: Similarly, if you overstate your expenses or claim deductions for which you are not eligible, you may have to pay back the excess deductions along with interest.

- Late Filing Penalties: If the inaccurate or incomplete Schedule Balance Sheet leads to a delay in filing your ITR-3 beyond the due date, you may also incur late filing penalties.

- Penalty under Section 271(1)(c): This section of the Income Tax Act imposes a penalty for concealing income or furnishing inaccurate particulars of income. The penalty can range from 100% to 300% of the tax sought to be evaded.

3. Reputation and Legal Implications:

- Loss of Credibility: Inaccurate reporting can damage your reputation and credibility with tax authorities and financial institutions.

- Legal Consequences: In extreme cases of fraudulent reporting, you may face legal action and prosecution.

Impact on Future Filings:

- Higher Scrutiny in Subsequent Years: Incorrect filing in one year can increase the likelihood of your returns being selected for scrutiny in subsequent years as well.

Mastering Your ITR-3 Schedule Balance Sheet: A Path to Financial Clarity and Compliance

Navigating the intricacies of the Schedule Balance Sheet in ITR-3 can seem daunting, especially with its evolving format and detailed requirements. However, armed with the knowledge and guidance provided in this comprehensive article, you're well-equipped to tackle this essential tax filing component with confidence.

Recap of Key Points:

- Who Needs to File: We've clarified the specific categories of taxpayers who are obligated to file the Schedule Balance Sheet – individuals/HUFs with business or professional income and partners in taxable firms.

- Understanding the Sections: We've meticulously broken down each section of the Schedule Balance Sheet – Source of Funds, Application of Funds, and No Account Case – explaining the purpose and specific details to be reported.

- Step-by-Step Guide: Our detailed instructions walk you through the process of filling each section accurately, ensuring consistency with your financial statements.

- Common Mistakes and How to Avoid Them: We've highlighted common pitfalls that can lead to errors and provided tips for accurate and complete reporting.

- Consequences of Incorrect Filing: We've emphasized the importance of accuracy by outlining the potential consequences of mistakes, from scrutiny to penalties.

Your Path to Success:

Accurate and timely filing of the Schedule Balance Sheet is crucial for maintaining compliance with tax laws and ensuring a smooth assessment process. By following the step-by-step guide, utilizing the expanded explanations, and referencing the additional tips, you can confidently navigate the Schedule Balance Sheet, even if it's your first time.

Remember:

- Professional Guidance: Don't hesitate to seek the expertise of a Chartered Accountant (CA) for complex situations or doubts. Their guidance can be invaluable in ensuring your tax filing is accurate and compliant.

- Organization is Key: Maintain organized financial records throughout the year. This will not only make filling the Schedule Balance Sheet easier but also be beneficial for your overall financial management.

- Timely Filing: Start the filing process early to allow ample time for review and correction of any errors. This will help you avoid the stress of last-minute filings and potential penalties for late submissions.

By embracing the insights and knowledge gained from this guide, you can transform the task of filing the Schedule Balance Sheet in ITR-3 from a daunting challenge into a manageable and even empowering process. It's a step towards greater financial transparency and compliance, ultimately contributing to the success and growth of your business or profession.

Disclaimer:

The information provided in this article is intended for general informational purposes only and should not be considered as professional financial or legal advice. While we have made every effort to ensure the accuracy and completeness of the information presented, tax laws and regulations are subject to change, and individual circumstances may vary.

It is strongly recommended that you consult with a qualified Chartered Accountant (CA) or tax professional before making any decisions or taking any action based on the information provided in this article. They can provide personalized guidance based on your specific financial situation and the most up-to-date tax laws.

We do not guarantee the accuracy, completeness, or timeliness of the information presented. We are not liable for any errors or omissions, or for the results obtained from the use of this information. Any reliance you place on the information in this article is strictly at your own risk.

This article is not a substitute for professional advice. It is essential to conduct your own research and due diligence before making any financial or tax-related decisions. We are not responsible for any losses, damages, or other liabilities incurred as a result of your use of this information.

By using this article, you agree to the terms of this disclaimer. If you do not agree with any part of this disclaimer, please do not use this article.

What's Your Reaction?